Here’s where Europe’s diversity becomes a liability.

PropTech Europe’s 2023 industry survey found that regulatory fragmentation forces companies to develop country-specific workflows, increasing development costs by 30-50%

What this means in practice:

- In France, digital property transactions must be processed through state-appointed notaries

- In Germany, private digital conveyancing platforms are allowed

- In Spain, cadastral data is publicly available

- In Italy, the same data is fragmented across regional offices with inconsistent formats

A PropTech vendor building a transaction platform for the EU market can’t build one solution. They must build 27 variants, each complying with national property law, data sovereignty rules under GDPR, and local certification requirements.

The result: scale economies never materialize. The “European market” is a myth for PropTech infrastructure.

The European reality: Why geography still matters

While the EU provides a unified regulatory framework on paper, implementation reality varies dramatically by country. This geographic fragmentation shapes both opportunities and barriers in ways that directly impact the integration tax.

The legacy infrastructure divide

Southern and Eastern Europe face the steepest technical debt. According to the European Real Estate Society, over 65% of social housing providers in Italy, Spain, and Poland still rely on custom-built on-premises systems developed before 2005 with minimal interoperability capabilities.

These aren’t edge cases. Social housing represents millions of units across these markets, all managed through systems that:

- Lack modern APIs

- Store data in proprietary formats

- Run on unsupported operating systems

- Cannot connect to cloud platforms without expensive middleware

Northern and Western Europe have different problems

Their systems are newer but equally fragmented. In Germany, the Federal Office for Building and Regional Planning reports that public housing agencies using pre-cloud infrastructure require costly middleware or manual data bridges, extending implementation timelines by 6-12 months

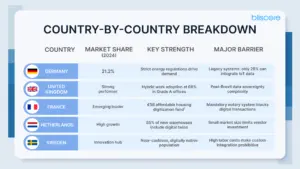

Germany: The Compliance-Driven Giant

Germany dominates at 21.2% market share , not through innovation but through regulation.

The Building Energy Act mandates digital energy monitoring for all large buildings by 2025 and deep retrofits for 180,000 properties annually

This isn’t optional. Non-compliance carries fines and restricts ability to lease commercial space.

The result: Germany now hosts over 6,000 new warehouse projects annually, each requiring smart facility management systems

These aren’t small installations, logistics facilities demand integrated systems for temperature monitoring, automated inventory tracking, and real-time energy optimization.

But here’s the catch: most of this spending goes to compliance, not optimization. German firms buy PropTech because they must, not because they’ve solved the integration challenge.

France: Public Sector as Catalyst

France took a different path: government-funded modernization at scale

Over 800,000 residential units received smart home kits under the MaPrimeRénov scheme between 2021 and 2023

That’s not a pilot program, it’s an industrial-scale deployment.

The Tertiary Decree adds teeth: large commercial buildings must reduce energy use by 60% by 2030 relative to 2010 levels, enforced through continuous digital monitoring. Landlords who miss targets face restricted leasing rights.

This creates a massive addressable market, but with French characteristics: centralized procurement, mandatory notary involvement in transactions, and strict interpretation of GDPR that restricts cross-border data flows.

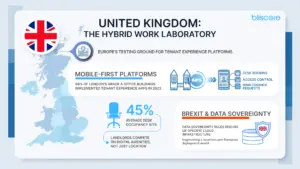

United Kingdom: The Hybrid Work Laboratory

Post-pandemic, the UK became Europe’s testing ground for tenant experience platforms.

68% of London’s Grade A office buildings implemented tenant experience apps in 2023: desk booking, access control, maintenance requests, all integrated into mobile-first platforms. Average desk occupancy sits at 45%, forcing landlords to compete on digital amenities, not just location.

But Brexit created new complexity. Data sovereignty rules now require UK-specific cloud infrastructure, fragmenting what was once a seamless pan-European deployment model.

The Nordics: Small Markets, Big Innovation

Sweden and the Netherlands punch above their weight through cultural factors: near-universal digital literacy, cashless economies, and populations comfortable sharing building usage data.

In the Netherlands, 85% of new distribution centers commissioned in 2023 included digital twin models and automated energy systems

Amsterdam’s Circular Buildings Program requires real-time space and user satisfaction tracking in all commercial developments.

Sweden’s approach is even more aggressive: the Environmental Protection Agency mandates that all new commercial buildings over 2,000 square meters use AI-driven energy models to achieve BREEAM certification.

The problem? Market size. With populations under 20 million, vendor economics struggle. International platforms invest in Germany and France first, leaving Nordic markets to rely on local startups that lack resources to scale.