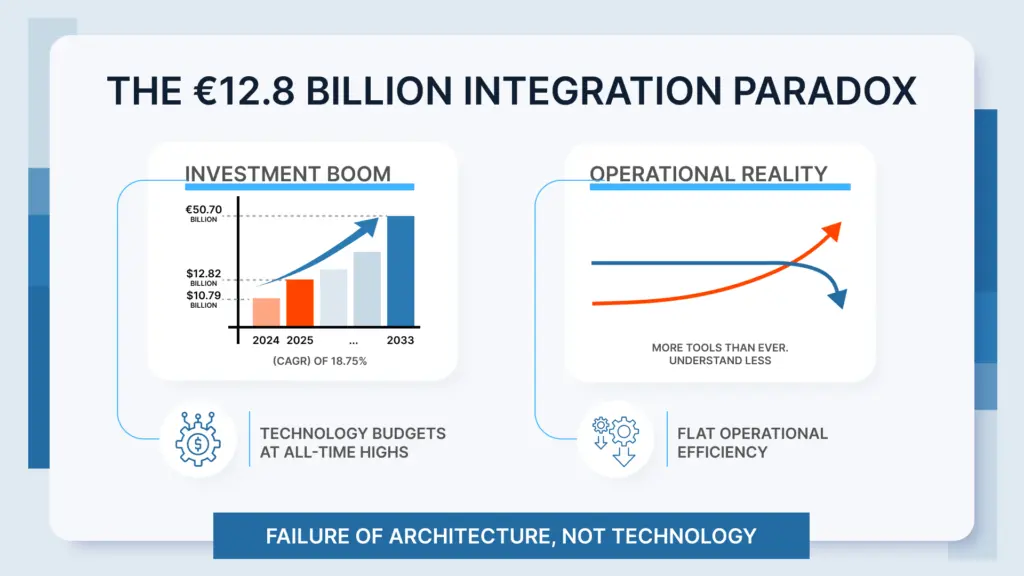

The €12.8 billion integration paradox: Why European Real Estate tech stacks are breaking under their own weight

There’s a strange conversation happening in European real estate boardrooms right now. Technology budgets are at all-time highs. By the end of 2025, the European PropTech market was valued at approximately USD 12.82 billion, up from about USD 10.79 billion in 2024, confirming a strong and sustained investment momentum in digital real estate solutions. This growth trajectory is projected to reach €50.70 billion by 2033, with a compound annual growth rate (CAGR) of 18.75%¹. Digital transformation is no longer optional.

And yet, when you ask operational leaders how they feel about their technology landscape, you hear the same refrain: “We have more tools than ever. We understand our business less than before.”

This isn’t a failure of technology. It’s a failure of architecture.

The 2025 market data tells a story the industry doesn’t want to hear: massive investment growth alongside stubbornly flat operational efficiency. What went wrong?

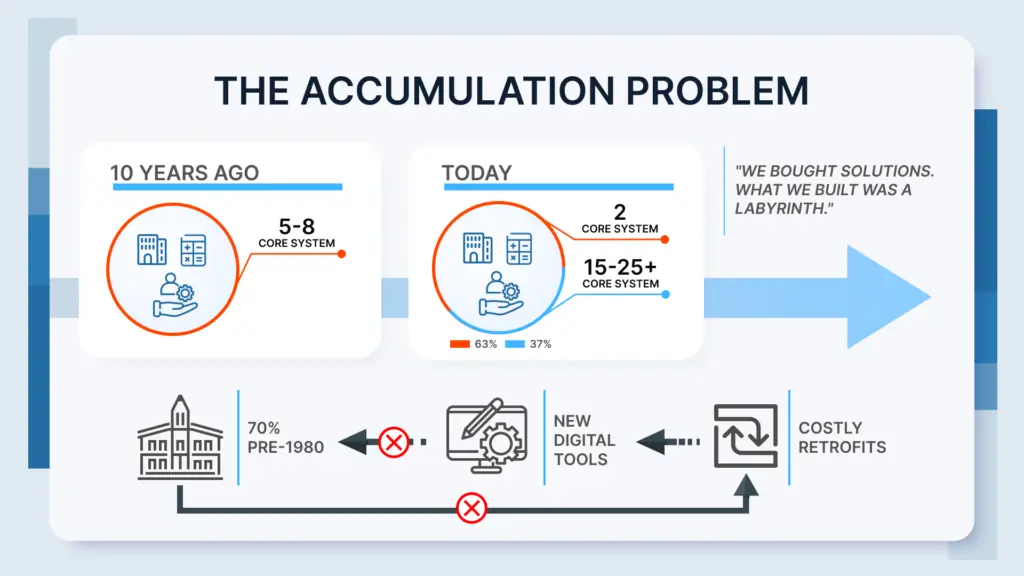

The Accumulation Problem: from platform to patchwork

Ten years ago, a typical commercial real estate firm operated with 5-8 core systems. Property management, accounting, maybe a CRM, some spreadsheets.

Today? 63% of real estate firms now use at least two software tools for property operations, but the reality is often far worse because many operate with 15-25+ systems.

Here’s what that looks like in practice:

- CRM for client relationships

- PMS for property operations

- ERP for financials

- Tenant experience platform for engagement

- Energy monitoring for utilities

- ESG reporting suite for compliance (critical now that real estate accounts for 37% of global CO2 emissions⁷)

- BIM software for building data

- Digital twin platform for visualization

- Predictive maintenance for assets

- Analytics dashboard (or three)

- Blockchain tools for tokenization and fractional ownership

Each was purchased to solve a real problem. Each vendor promised seamless integration. Each lived in its own silo.

One head of operations described it this way: “We bought solutions. What we built was a labyrinth.”

The problem runs deeper than tool sprawl. According to Eurostat, 70% of Europe’s building stock was constructed before 1980⁹, lacking modern energy and data infrastructure. This creates a vicious cycle: new digital tools can’t extract value from old buildings without costly retrofits, but retrofits can’t be justified without proving ROI through… digital tools.

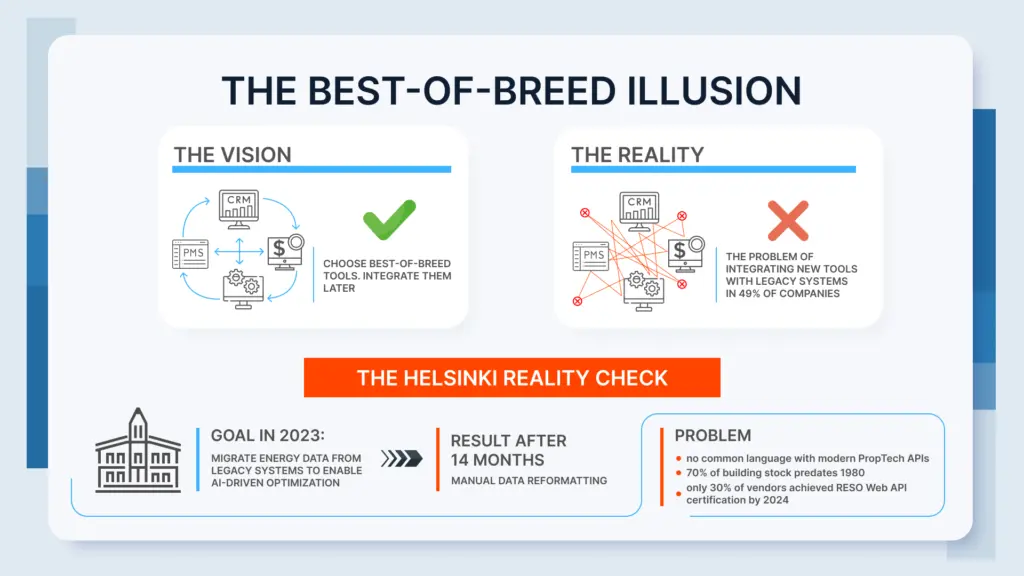

The best-of-breed illusion

The industry mantra for the past decade was simple: “Choose best-of-breed tools. Integrate them later.”

It made sense. Why settle for a mediocre all-in-one platform when you could cherry-pick the best CRM, the best PMS, the best analytics engine?

The hidden assumption was that integration would be straightforward. That APIs were truly open. That data models would align. That business logic could flow seamlessly between systems.

None of that proved true at scale.

The Helsinki reality check

Consider a cautionary tale from Northern Europe. In 2023, the City of Helsinki attempted to modernize its municipal facility management. The goal was simple: migrate energy data from legacy systems to enable AI-driven optimization.

The result? 14 months of manual data reformatting before AI optimization could even begin.

This wasn’t incompetence. It was the European reality: 70% of building stock predates 1980, and the systems managing them reflect that era. When Helsinki’s 1990s facility management platform encountered modern PropTech APIs, there was no common language. Building identifiers didn’t match. Energy readings used inconsistent units. Historical data lacked timestamps that modern analytics require.

The project eventually succeeded, but only after dedicated teams manually reconciled decades of inconsistent data at a cost that exceeded the original software licenses by 400%.

This pattern repeats across Europe. What actually happened when firms pursued best-of-breed:

- Vendor APIs changed without warning

- Data definitions conflicted (What counts as “active tenant”? Depends which system you ask)

- Micro-integrations broke during updates

- Business logic scattered across systems with no single source of truth

One firm discovered their energy platform and ESG reporting tool, both industry-leading, couldn’t reconcile building identifiers. Six months of manual reconciliation followed.

This is the reality facing the industry: 49% of real estate businesses report challenges integrating new software with legacy systems. More damning still, only 30% of vendors achieved RESO Web API certification by 2024¹¹, forcing firms into costly custom integrations that break with every update.

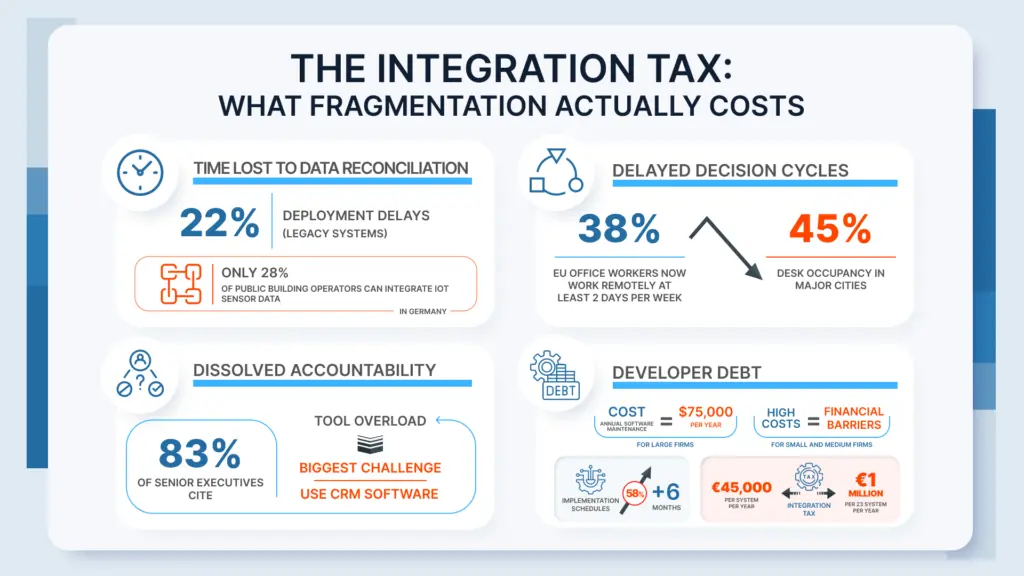

The integration tax: what fragmentation actually costs

The true cost of a fragmented stack isn’t visible in software licenses. It shows up in:

Time lost to data reconciliation

When tenant data lives in three places, someone has to reconcile it. Manually. Monthly. Integration with legacy systems accounts for 22% of deployment delays across the industry.

In Germany, only 28% of public building operators can integrate IoT sensor data into centralized dashboards due to incompatible infrastructure². The remaining 72% either maintain dual systems or rely on manual data transfers (processes that consume weeks of staff time every quarter).

Delayed decision cycles

You can’t act on what you can’t see clearly. When insights require pulling reports from five systems, analysis slows to a crawl.

Over 38% of EU office workers now work remotely at least two days per week, reducing average desk occupancy to 45% in major cities¹³. Yet most building operators can’t track real-time utilization because their access control system doesn’t talk to their booking platform, which doesn’t integrate with their energy management system.

Dissolved accountability

When a process spans six tools, who owns it? When something breaks, who fixes it? Answer: everyone, which means no one. 83% of senior executives cite getting staff to use CRM software as their biggest challenge¹⁴, a symptom of tool overload, not user resistance.

When employees face a dozen logins, conflicting workflows, and unclear data ownership, they revert to spreadsheets. The expensive PropTech stack becomes expensive shelfware.

Developer debt

The numbers here are brutal: annual software maintenance costs reach up to $75,000 for large firms, with 38% of small and medium real estate firms citing high costs as financial barriers.

But the hidden cost is worse: developer time. In Germany, 58% of PropTech implementations exceed initial schedules by six months or more due to lack of in-house skills for configuration and change management². This isn’t a training problem — it’s a structural one.

One CIO calculated their “integration tax”—the hidden cost of connecting disparate tools—at €45,000 per system per year. With 23 systems, that’s over €1 million spent just keeping tools talking to each other.

This is money that produces zero value. It’s the operational equivalent of paying rent on empty space.

The architecture problem no one wanted to see

European real estate just spent €12.8 billion learning an expensive lesson: you can’t buy your way out of an architecture problem with more tools. The best-of-breed strategy made sense. Pick the best CRM, the best PMS, the best analytics, integrate later, but “later” never comes.

Helsinki: 14 months reformatting data before optimization could start. Germany: 72% of operators are still moving data manually. One CIO: €1 million yearly just keeping 23 systems connected.

The industry bet that APIs would be open, data models would align, and systems would talk to each other. None of that proved true, especially when 70% of Europe’s buildings predate 1980.

By 2033, the market will hit €50.70 billion. The question isn’t whether firms will invesе; it’s whether they’ll keep making the same architectural mistake at scale.

The firms that win won’t have the most tools. They’ll be the ones who stopped asking “which tool solves this?” and started asking “what architecture eliminates this problem?”

Because right now, the industry is paying billions to make the same mistake faster.